Navigating Retirement with a 401(k)

May 18, 2024 By Susan Kelly

A 401(k) retirement savings plan is a very important financial tool for numerous Americans, giving them a way to save money with tax benefits set aside for their future. Knowing the mechanism of how a 401(k) functions and its different parts becomes crucial in planning effectively for retirement.

Understanding 401(k) Basics

A 401(k) is a retirement savings plan offered by an employer. It permits employees to put some of their salary into this tax-deferred investment account through payroll deductions. These contributions are taken out from the employee's paycheck before any taxes are withheld, resulting in a reduction of their taxable income for that year.

Employers could also give matching contributions, which increase the total amount saved for retirement by an employee. Apart from tax benefits, a 401(k) usually provides the option for workers to adjust their contribution amounts according to their money matters and retirement objectives.

- Customizable contributions: Employees can adjust their contribution amounts to align with their financial goals and circumstances.

- Employer-sponsored: 401(k) plans are established and sponsored by employers, providing a convenient way for employees to save for retirement through automatic payroll deductions.

Exploring Contribution Limits and Tax Benefits

The amount you can contribute to a 401(k) every year is limited by the IRS. In 2024, individuals below the age of 50 can contribute up to $20,500 yearly while those who are 50 years or older have a catch-up contribution limit of an extra $6,500. The main advantage of having a 401(k) is that it provides tax benefits. Contributions are made before taxes, which decreases the individual's taxable income in that year.

Also, the 401(k) account lets investment earnings grow without any taxes until they are withdrawn at retirement time. Additionally, it is good for people to note that they can't carry over any unused contribution limits from one year to another. This highlights the need to make maximum contributions every year so as not to miss out on tax benefits completely.

- Annual contribution limits: Contributions to a 401(k) plan are subject to annual limits set by the IRS, which can vary based on age and other factors.

- Use-it-or-lose-it: Contribution limits do not roll over from year to year, so individuals should aim to maximize contributions annually to optimize tax benefits.

Employer Matching Contributions

Matching contributions from employers are given to encourage employees to join the 401(k) plan. The amount that an employer matches can differ, but it often falls between 3% and 6% of the employee's salary. For instance, if an employee contributes 3% of their salary to their 401(k) plan and the employer offers a match rate at this level too, then the total contribution becomes equivalent to 6% of what they earn every year.

Employer matches are like getting free money because they increase the total amount of funds in an employee's retirement savings. This is a very useful benefit. In addition, you may find that employer matches are usually tied to a vesting schedule. This plan decides when workers get complete ownership of the money matched by their bosses.

- Vesting schedules: Employer matching contributions may be subject to vesting schedules, determining when employees gain full ownership of those funds.

- Free money: Employer matches provide additional retirement savings at no cost to the employee, enhancing the overall value of the 401(k) plan.

Understanding Investment Options

401(k) plans normally have a variety of investment selections, so the person taking part can decide where they want their contributions to be invested. Regular choices for investing could be mutual funds, index funds, exchange-traded funds (ETFs), and target-date funds. People participating in the 401(k) plan can distribute their contributions among these investment options according to what suits them best about risk level acceptance, aims for investing, and time remaining until retirement.

Moreover, people who take part in these plans must keep on checking and modifying their investment distributions. This is done to make sure that the way they are putting money into different options matches up with their financial aims and how much risk they can accept. Periodic balancing of investments might be useful for keeping a variety of assets in a portfolio and controlling risk efficiently.

- Portfolio diversification: Participants can diversify their investment portfolio by allocating contributions among different asset classes, reducing overall risk.

- Regular review: Periodic review and adjustment of investment allocations help ensure that the portfolio remains aligned with changing financial goals and risk tolerance.

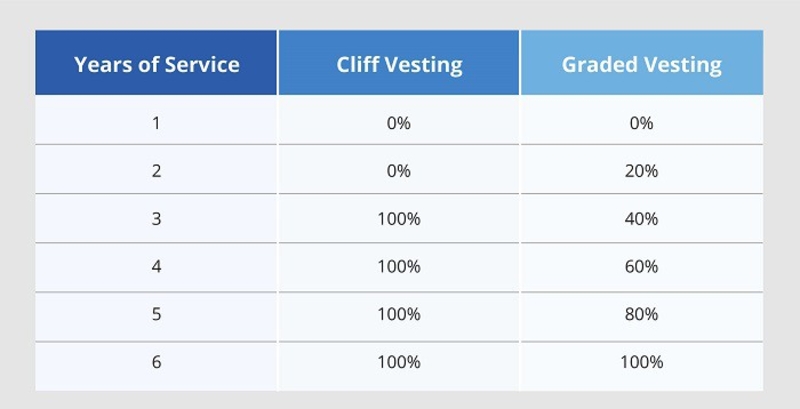

Navigating Vesting Schedules

The contributions made by an employer into a 401(k) plan can sometimes be under the control of a vesting schedule. This schedule sets out when employees officially own these contributions. Vesting schedules are different for every employer but usually go from immediate vesting to a graded system where ownership is gained over some years of service. Employees must comprehend their employer's vesting schedule so they can make the most of the benefits offered through matching contributions from employers in this retirement savings account called 401(k) plan.

Additionally, people who are part of a retirement plan might find it helpful to know that employer contributions usually get forfeited if they quit the company before becoming fully vested. This knowledge about how vesting schedules work could affect choices related to switching jobs and planning for retirement.

- Forfeiture of unvested contributions: Employer contributions that are not fully vested may be forfeited if the employee leaves the company before reaching full vesting.

- Impact on retirement planning: Vesting schedules can impact retirement planning strategies, influencing decisions regarding job changes and the timing of retirement.

Planning for Retirement with a 401(k)

401(k) is an important tool to plan for retirement. It gives benefits like tax savings, matching from the employer, and different investment options. People who use it can build a strong financial future by knowing how 401(k)s work and using their advantages well. Regularly checking and changing the amount put into a 401(k), along with where money is invested, helps make sure that it still matches the long-term money goals of a person.

Complete Guide: How To Report and Pay Independent Contractor Taxes?

Dec 05, 2023

When making their tax payments, employees have a reasonably easy time. Taxes are deducted by their employer from each paycheck, and the proceeds are remitted to the appropriate governmental authority. Employees have to pay taxes on their income as earned, and they typically expect to receive a return when it comes time to file their taxes. Paying taxes is not as straightforward for independent contractors as it is for employees of corporations.

Penny Stocks to Watch in Q3 2022

Nov 20, 2023

There's been a lot of volatility in the stock market since the beginning of 2022. Investors are split between protecting themselves and taking advantage of the possibilities in the current economic climate. Despite the economy's current state, a plethora of attractive investments can be made right now.

Different Features of InCharge Debt Solutions

Dec 07, 2023

Three million clients have received assistance from InCharge Debt Solutions in consolidating and paying off their debts. They are a 501(c)(3) nonprofit organization that was established in 1997 with the primary mission of assisting customers in the establishment of debt management strategies.

Is Chesapeake Life Insurance Right for You? An In-Depth Review

May 09, 2024

Explore why Chesapeake Life Insurance, with its comprehensive coverage options and solid financial backing, may be the ideal choice for your life insurance needs.

Avoid Capital Gains Tax on Your Asset Property

Nov 20, 2023

Match defeats Investors can take losses to balance out and offset their gains for a given year. Savvy investors collect capital losses as they happen and use them to reduce their present and future tax obligations. Extra losses that aren't applied to gains can be used to offset ordinary income up to $3,000 in total.

When Is The Best Time To Invest

Oct 14, 2023

Want to maximize your profits and minimize risk when investing? Here's a comprehensive guide to determining the best time to invest in stocks, bonds, and mutual funds.

Single-Premium Life Insurance Explained: Everything You Need to Decide

May 14, 2024

Discover if single-premium life insurance is right for you. Learn its pros, cons, and factors to consider in this guide.

Mortgage Interest Rates Forecast: A Review

Dec 23, 2023

The average interest rate for a 30-year stabilized mortgage hit its highest level in 20 years in the first few days of November, and it's likely to keep going up this month. Experts on mortgages still talk about inflation and how the Federal Reserve is trying to stop it. Prices at the store are 8.2% higher than they were a year ago. In response, the Federal Reserve raised its key interest rate for the sixth time this year.

Understanding Home Appraisals

Jan 13, 2024

Have you ever wondered why home appraisals are so important? Read on to find out how home appraisals can affect your ability to purchase a new property and get tips for getting the most out of yours.

What Should be your Financial To-Dos in your 20s?

Nov 08, 2023

It's important to make wise financial choices in your twenties since they can affect your life for decades. Incorporate these suggestions into your current routine to ensure your long-term effectiveness.

Legal Status of Airbnb in Major Cities

Jan 25, 2024

Airbnb is a popular choice among thrifty vacationers since it is a short-term rental business that allows property owners as well as renters to earn extra money by renting out their homes to other guests. On the other hand, it might be a difficult task for regulatory bodies all over the globe.

Best Place to Buy Used Furniture Estate Sales

Feb 25, 2024

Looking for used furniture on a budget? Learn why estate sales are one of the best options and gain access to tips that will make it an easy shopping experience.